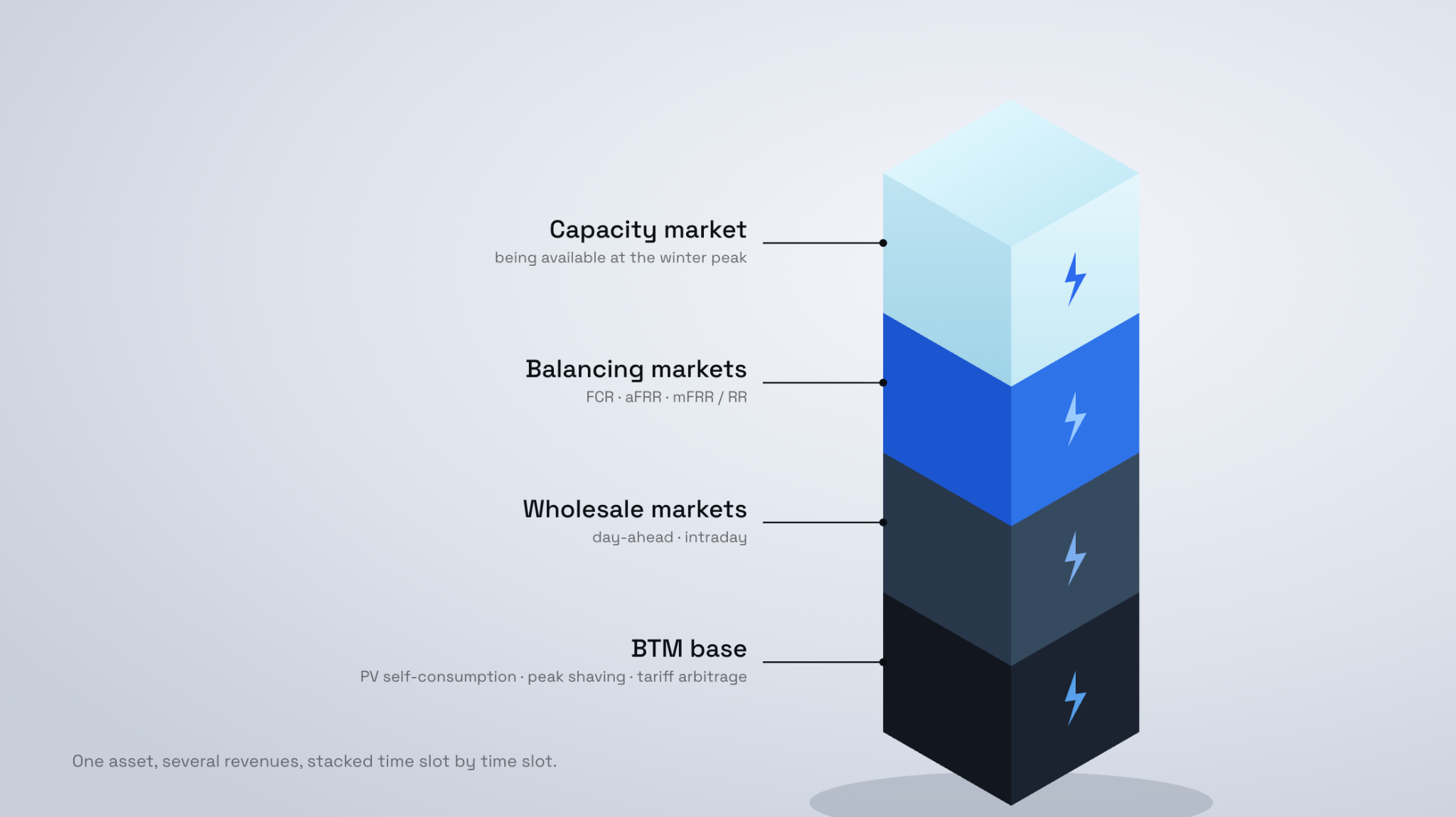

Value stacking: how a battery layers up its revenues

A storage battery is not a "single-revenue" asset. Quite the opposite: its profitability rests on its ability to serve several markets at once, often within the same day. This is what we call value stacking.

The challenge is not merely to pick the "best" market, but to optimise value stacking across all available revenue streams: maximising total revenue under physical constraints (a MWh can only be sold once) and regulatory ones. It is an optimisation problem, and that is precisely what the Tilt Energy platform does.

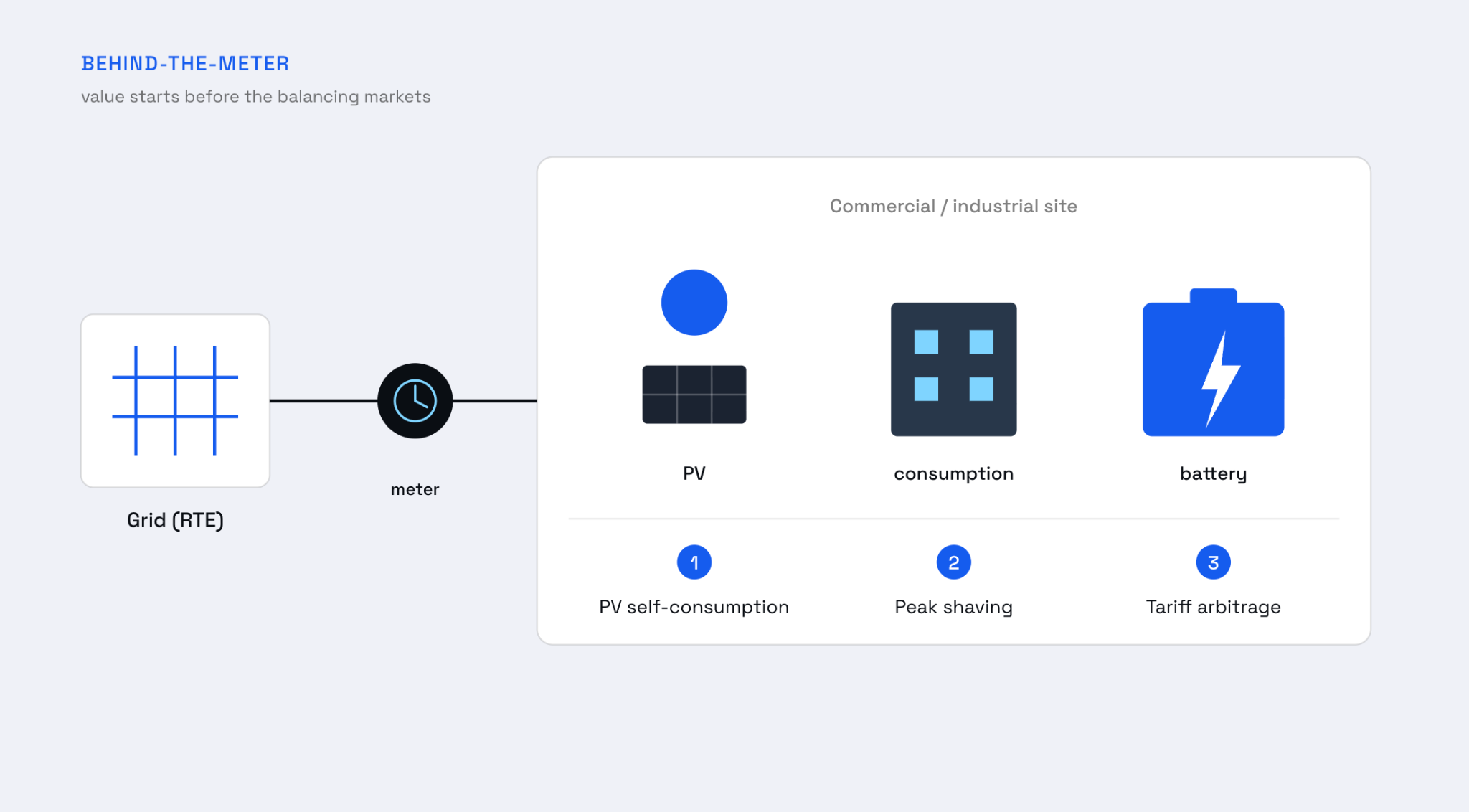

To illustrate how this works in practice, let's start from the battery installed behind the meter (Behind-The-Meter, BTM) of a commercial or industrial site, and work our way up, layer by layer, to RTE's markets.

1. The BTM building block: optimise the site before looking at the markets

Even before talking about national balancing markets, a battery installed at a customer's site generates value by optimising its own electricity bill. This value is driven by three key mechanisms.

Optimising photovoltaic self-consumption

On a site equipped with solar panels, midday output often exceeds instantaneous consumption. Without a battery, this surplus is either fed back into the grid at low value or lost. The battery stores the PV surplus to release it at the end of the day, when the site is consuming and solar no longer produces. This raises the self-consumption rate, and every self-consumed kWh is a kWh not bought from the supplier (at full price, including TURPE and taxes).

Optimising subscribed power (peak shaving)

Network charges (TURPE in France) depend largely on subscribed power. A site that draws during large peaks pays dearly, both in its subscription and in overrun penalties. The battery shaves these peaks (peak shaving), meaning that it discharges exactly when power consumption peaks, allowing a lower subscribed capacity and a smoother withdrawal profile. The savings are structural and recurring.

Optimising the supply-contract tariff

The energy price on a supply contract is not constant: peak/off-peak hours, mobile peak, spot exposure. The battery arbitrages these windows: it charges when energy is cheap and discharges when it is expensive. This is a purely "internal" arbitrage within the contract, with no interaction with wholesale markets, but it is often the first revenue layer of a BTM project.

These three levers share one trait: they require no particular market role. They are the foundation. Value stacking truly begins when you open the battery onto the markets.

2. Trading on wholesale markets: yes, it works in BTM

You often hear that trading is reserved for large "front-of-meter" assets. That is false. A BTM battery can perfectly well monetise energy on wholesale markets:

Day-ahead (D-1): you buy/sell energy for the next day, hour by hour, playing on the differential between low and high hours. The day-ahead "spread" (the gap between the most expensive and the cheapest hour) is one of the key indicators of arbitrage value.

Intraday (D): you adjust the position in near real time to capture the volatility of the day itself.

The key, in BTM, is NEBCO (Notification of Exchange of Consumption Blocks). This is the mechanism that lets you monetise on wholesale markets the energy blocks curtailed or consumed by an asset located behind the meter, without being the site's supplier. In practice, the aggregator declares the blocks, the site's supplier is compensated for the mismatch, and the captured arbitrage value flows back to the asset owner. This is what opens wholesale trading to a BTM battery, a value pool often overlooked on this type of installation.

3. The core of the value: balancing reserves

This is where most of the value for a battery lies today. To keep grid frequency at 50 Hz at all times, RTE continuously procures reserves, at nested time scales. A battery, thanks to its near-instant responsiveness, is an ideal asset to provide them.

FCR: primary reserve FCR (Frequency Containment Reserve) is the fastest: activation within seconds, symmetric, to immediately contain any frequency deviation. It is remunerated on available power, whether activated or not. In practice, it remains mostly the preserve of large batteries: the required instrumentation (frequency meter, qualification) carries a fixed cost that is hard to amortise over small assets, and the market is currently somewhat saturated (though less so since March 2026, but with remuneration still below aFRR), so the game often isn't worth it for a diffuse BTM fleet.

aFRR: secondary reserve aFRR restores frequency automatically once FCR has handed over. It pays on two components: capacity (being available) and energy (being effectively activated). Since the move to pay-as-cleared, the price forms at the marginal accepted cost, which has appreciably improved its value. It is today the most lucrative market for batteries, and therefore the first revenue pool targeted in a stack. aFRR also shows strong seasonality (typically more lucrative in summer than in winter on the capacity component), which makes temporal optimisation all the more decisive.

mFRR / RR: tertiary reserve mFRR and RR (tertiary reserves, activated manually by RTE) act more slowly, to rebuild the secondary reserve or offset a forecast deviation. They are historically better suited to "energy" assets than to short-duration batteries, but remain a usable building block depending on storage configurations.

The key point: these reserves cannot be stacked freely with each other at a given moment. Power committed to FCR is not available for aFRR at the same time. Value stacking therefore consists of intelligently allocating power and storage between reserves, arbitrage and self-consumption, slot by slot.

4. MECAPA: being paid to be available at the peak

The capacity mechanism (MECAPA) remunerates the mere fact of being available during system-stress periods (the "PP", peak periods), independently of any activation. For a battery, it is a complementary capacity revenue that stacks on top of everything else.

The new regime sets aside a dedicated volume for low-carbon flexibilities (on the order of 4.7 GW) and targets tightened peak windows (typically the morning and evening slots in winter). It is a direct window of opportunity for storage and load control.

Stock-constraint coefficient and technology coefficient

This is where the two coefficients every battery operator must understand come in, because they determine the power actually monetisable under the mechanism.

The stock-constraint coefficient (Kj) reflects a physical obvious truth: a battery cannot hold its full power indefinitely. The lower its autonomy (storage duration), the more its contribution is "derated"; a long-duration battery counts for nearly 100% of its power. Concretely, RTE's lookup table gives tiers on the order of:

1 h → 0.35 · 2 h → 0.58 · 3 h → 0.75 · 4 h → 0.86 · 5 h → 0.97 · 6 h → 1.00

The effect is massive: a battery with 2h of storage monetises only a little over half its power, whereas one with 5–6h captures nearly all of it. It is an important sizing trade-off, to factor in from project design onwards.

The technology coefficient (C_filière) does not depend on storage duration but mainly on the technology: it accounts for the heterogeneity of contributions across technology sectors and corrects the partial representativeness of the failure landscape of PP hours. The battery sector has a technology coefficient of 0.55 (not applied to BTM batteries on a withdrawal-only site).

The capacity level monetised is therefore built, in simplified terms, as:

Available power × stock coefficient × technology coefficient

5. The roles to hold with RTE

Value stacking requires taking on, or having an aggregator carry, several market roles with RTE. This is an often underestimated point, and one of the locks Tilt removes for its clients.

Balance Responsible Party (RE / BRP): responsible for the injection/withdrawal balance of its perimeter. Indispensable to obtain market access from an exchange (EPEX, Nord Pool) and thus to participate in the Day-Ahead and Intraday spot markets.

BSP (Balancing Service Provider): the generic term that, on the French side, covers several distinct roles depending on the market addressed:

- demand-response operator (opérateur d'effacement): to monetise consumption curtailments via NEBCO;

- balancing actor (acteur d'ajustement): to participate in mFRR (MA, MARI, RR);

- reserve provider (responsable de réserve): to certify assets and provide aFRR;

- scheduling agent (responsable de programmation): indispensable to be a reserve provider.

TPC (Certification Perimeter Holder): to monetise capacity on MECAPA, it must be certified and declared in the mechanism.

Holding these roles, ensuring their technical compliance (metering, telemetry, qualification tests, certification) and their daily optimisation represents a real barrier to entry. This is what an aggregator pools.

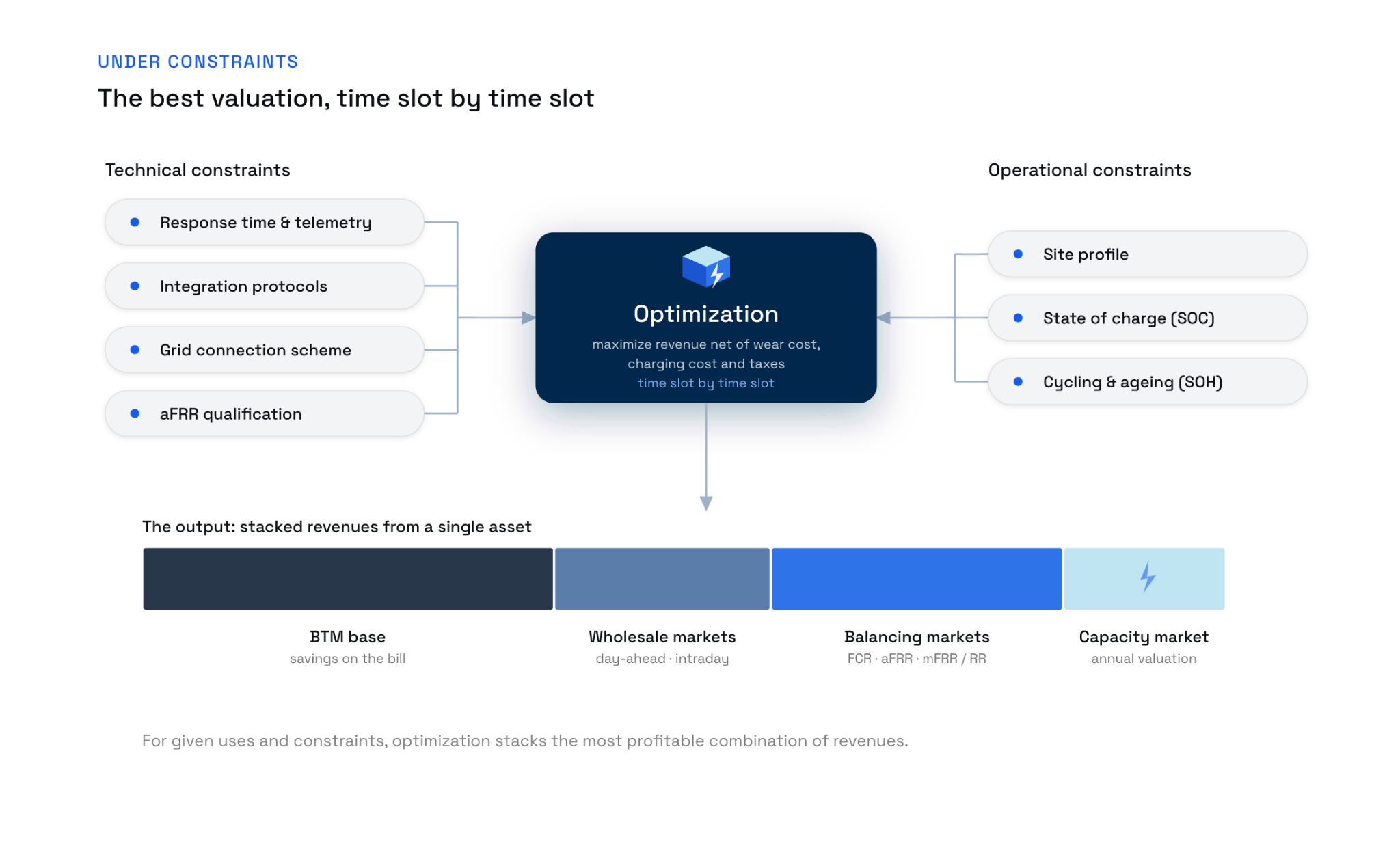

6.The constraints that shape everything

Value stacking doesn't happen "for free". Two families of constraints frame the optimisation.

Technical constraints:

- Response time and telemetry: reserves demand activation within minutes/seconds and real-time monitoring imposed by RTE.

- Integration protocols: control of batteries and assets via Modbus, MQTT or REST API depending on the equipment (integration quality conditions activation reliability).

- Connection scheme: it determines whether the battery can inject onto the grid or only serve behind the withdrawal meter, which opens or closes part of the markets.

- Asset certification and qualification (aFRR): before it can sell aFRR, each asset must be certified by RTE (activation tests, response-dynamics verification, compliant telemetry).

Operational constraints:

- Site consumption/production profile: it bounds the entire BTM stack. The site's withdrawal conditions the potential, the PV surplus feeds self-consumption, and capacity depends on the connection. The same MW of battery isn't worth the same thing depending on the site hosting it.

- State of charge (SOC): you can't sell an upward reserve if the battery is empty, nor a downward one if it is full. Managing SOC by anticipating the commitments made on each market is at the heart of operations.

- Cycling and ageing (SOH): each cycle wears the battery. Aggressive dispatch can erode the manufacturer's warranty. Optimisation must therefore value not only instantaneous revenue but the marginal cost of wear.

7. Why it's an optimisation problem, and what Tilt does

Let's recap. At a given moment, the same battery can lay claim to:

- self-consuming PV,

- shaving the site's power peak,

- arbitraging the contract's tariff windows,

- trading on day-ahead / intraday,

- providing FCR, aFRR, mFRR,

- being available for MECAPA.

But these uses are partially competing: power committed here is no longer available there, storage emptied for an arbitrage is no longer mobilisable for a reserve, and each cycle has a cost. The question is therefore never "which market?" but "which allocation of power and storage, slot by slot, maximises revenue net of wear costs, loading costs, and taxes?".

This is a multi-market co-optimisation problem under constraints, exactly what the Tilt Energy platform solves. Its algorithms continuously control and activate thousands of assets (batteries, building management systems, HVAC, heat pumps, EV chargers) spread across hundreds of sites, arbitraging in real time between all these value pools. Tilt holds the necessary RTE roles, ensures technical compliance, and maximises the monetisation of flexibility without compromising on the site's use or comfort.

Value stacking is not a marketing option: it is the very condition of a battery's profitability today. And it is captured only with the right roles, the right integrations and the right control intelligence.